U.S. Energy Industry Trends To Watch In A 2025 Trump Presidency

New Trump administration policies will impact the energy industry, but maybe not in the ways Trump supporters expect, writes Guest Contributor Allan Marks.

Allan Marks is a partner at Milbank LLP and a lecturer at UC Berkeley School of Law and UCLA School of Law. This article was originally published in Forbes, for which he is a contributor, on November 7, 2024.

When Donald Trump returns to the Oval Office in January 2025, his second presidency will have widespread implications for the energy industry, especially new investments, but not necessarily in the ways his supporters might expect.

A renewed emphasis on fossil fuels is expected under another Trump administration, though coal will likely remain moribund thanks to poor economic fundamentals and constrained access to capital. Investment across the energy spectrum –from oil and gas and renewables to energy storage and transmission – could well increase due to growing power demand, incentives for new supply, and permitting reforms, extending existing trends from the past four years. Because of backsliding on the energy transition, increased greenhouse gas emissions and resulting harm from climate change will accelerate, with devastating impacts in the United States and around the globe.

Nonetheless, potential policy changes in three areas could undercut new energy investment under a second Trump administration: protectionist trade measures and deglobalization; regulatory uncertainty and political risk; and fiscal and monetary policy.

Renewable Energy Vs. Fossil Fuels

Renewables or fossil fuels? Politicians and pundits put them at odds during the 2024 presidential campaign, but the tension was overblown. For better or worse, investment in fossil fuels represents more continuity than change. U.S. fossil fuel production rose over the last four years, from 76 quads in 2020 to a record high of 86 quads in 2023, over ten times the amount of total renewable energy production, according to the U.S. Energy Information Administration.

Vice President Kamala Harris campaigned in 2024 on support for gas fracking as well as renewable energy. President Joe Biden granted almost 50 percent more oil and gas drilling permits for wells on federal land than did former President Donald Trump, according to data through 2023 from the Interior Department’s Bureau of Land Management reported by POLITICO Pro. Despite Biden’s raising royalty rates for new fossil fuel drilling leases on federal land for the first time in a century and his temporary pause in approving licenses for new LNG export terminals, gas production continues to boom, and LNG exports have increased substantially.

Some of that increase reflects the significant expansion of LNG exports to Europe following Russia’s invasion of Ukraine, but these are longstanding trends under both parties. Over the past two decades, again according to EIA data, total domestic energy consumption has been basically flat thanks to efficiency gains, but total fossil fuel production has grown by over 34% and exports have grown by over 150%, making the United States a net energy exporter every year since 2019.

This trend of increased fossil fuel output is expected to continue under Trump so long as demand remains robust. But the president has little control over drilling activity, rig counts, or new exploration and production of oil and gas, most of which is on private not federal lands. He might relax enforcement of environmental rules or seek new subsidies for fossil fuels. Trump vociferously favors fossil fuels and has criticized renewables, especially wind power and electric vehicles.

But renewables have powerful corporate champions and trade associations with support across the aisle in Washington, D.C. Some of Trump’s most ardent political backers, like Elon Musk, depend on existing federal subsidies (expanded under the Inflation Reduction Act) for EVs assembled in North America and for EV charging infrastructure, and investors in crypto currencies who supported Trump’s campaign need plenty of new power-hungry data centers.

Renewables are essential to meeting the reliability, affordability and sustainability goals of state regulators and grid operators. State policies – like renewable portfolio standards, resource adequacy requirements, and transmission planning – create tailwinds for renewables even in the absence of federal incentives.

Renewable energy already provides reliable power with significant grid penetration at a levelized cost of energy that is comparable to or lower than gas or coal. Massive investment in added renewable energy and storage capacity in Texas, California and other states will continue, even as natural gas fired power plants are added or retained to replace more expensive, obsolescent coal plants and to meet the massive growth in baseload power demand from AI-driven data centers and other digital infrastructure.

The maturity and low cost of renewable energy mean that the trend toward increased investment in renewables will continue even with an uptick in fossil fuels. Wind power, solar energy, and battery storage together make up over 95% of the new or planned projects currently seeking grid interconnection nationally, with natural gas accounting for the remainder, according to Lawrence Berkeley National Laboratory. The energy incentives in the IRA, likely to remain in place, favor more than just renewables like wind and solar power. Natural gas and nuclear power also benefit from IRA tax incentives, as do domestic manufacturing and clean energy jobs.

Gas and renewables often go hand in hand. Cheaper natural gas makes it less costly to increase the use of intermittent renewable energy and may enhance grid reliability and flexibility in markets with rising power demand. The “all-of-the-above” energy strategy touted by Trump during the campaign, in practice also followed by the Biden-Harris administration for the past four years, may well expand.

Inflation Reduction Act Is Here To Stay

The IRA, and specifically the tax credits for energy investments and production, is unlikely to be repealed. No Republicans voted for its enactment in 2022, which passed on party lines. It is considered Biden’s landmark achievement on energy, climate, and industrial policy. Yet, the law’s energy incentives are popular in many Republican districts, especially those hurt by job losses or plant closures as the coal industry has declined since the early 2000s. Coal has declined in part due to stricter air emissions requirements, but mostly because natural gas and renewables have become much cheaper. The IRA gives projects in energy-impacted communities bonus tax credits.

The nonpartisan business and clean energy advocacy group E2 reported in August 2024 that “red” states and Republican congressional districts have disproportionately benefitted from the IRA. They calculated that more than half of all projects were in Republican districts, that 19 of the top 20 congressional districts for clean energy investments are held by Republicans, and that nearly 40 percent of all U.S. congressional districts are home to at least one announced project. The 334 projects announced under the IRA in 40 states have created 109,278 jobs and brought $126 billion in private investments in the law’s first two years.

That is why 18 members of the House Republican Conference wrote a letter on August 6, 2024 to House Speaker Mike Johnson asking him not to seek repeal of the IRA. In particular, the Republican Congressmembers stated, “Energy tax credits have spurred innovation, incentivized investment, and created good jobs in many parts of the country – including many districts represented by members of our conference.”

Under the IRA and other laws enacted by Congress under the Biden-Harris administration, the Department of Energy and other departments have advanced billions of dollars to fund clean hydrogen, advanced nuclear, basic and applied energy research, EV charging networks, water and water treatment projects, transit and port upgrades, and other innovative infrastructure technologies or projects. The new Trump administration may not pursue these policy goals, and mitigating climate change is certainly not going to be a priority. Negotiations on the 2025 tax bill will implicate many of the IRA’s provisions. But IRA incentives for energy investment – especially onshoring manufacturing and blue hydrogen and carbon capture, sequestration and storage, which are supported by natural gas companies – may well survive.

Trade Policy And Deglobalization

Trump shares Biden’s priorities to bring manufacturing onshore and to stymie imports especially from China. These policies bolster domestic supply chains but also add significant costs. Cost hikes would be exacerbated, and existing supply chains could be significantly disrupted, by broader economy-wide protectionist tariffs or other trade barriers. Tariffs could slow domestic investment and contribute to inflation. Trade policy also impacts fiscal policy, discussed below. Trade wars combined with geopolitical disengagement could lead to deglobalization that hurts the economy even if domestic manufacturing grows.

Will deglobalization boost U.S. energy investment? Likely not. Trade barriers will meet with countermeasures in other countries, including the European Union and Asian markets. Tit-for-tat trade impediments could depress U.S. exports while making imports more expensive, functioning essentially as a tax on consumers and global businesses.

Deglobalization is an energy issue, not just a trade issue. Energy investments from Indiana to India and Texas to Thailand depend on liberal policies for the movement of more than equipment and natural resources. Cross-border capital flows, technology transfer (and respect for intellectual property ownership rights), and migration of skilled labor underpin energy sector investment across the United States as they do in other developed markets and especially in emerging markets. Nationalist or protectionist policies that jeopardize the (relatively) free movement of capital, goods and services impede investment and raise costs.

Regulatory Uncertainty And Political Risk

Energy is a quintessentially global business. Two obstacles could undermine investor confidence in the United States as a place to invest: regulatory uncertainty and political risk.

For a major equity sponsor to approve a final investment decision for a new project, and for large banks and institutional investors or private credit funds to commit to lend, they need confidence in future cash flows. The timing and certainty of completing construction on a new project within budget, and the amount, timing, and volatility of forecasted revenues and operating costs, dictate whether a project is financially viable. That predictability depends on market factors and macroeconomic stability.

Today, there is ample available capital. Liquidity is high, and both the inflation rate and the cost of capital are coming down. The labor market remains remarkably healthy, based on the unemployment rate, labor force participation, quits and job openings, and persistent real wage growth. For the next year at least, the new president inherits a solid economy.

So, for investors in new energy and infrastructure projects, the main constraint is not liquidity. Rather, the main factors impeding new projects are permitting delays and, for new power generation or energy storage projects, obtaining grid access and reliable transmission capacity.

The prospects for permitting reform that further streamlines the process at the federal level are strong, building on the permitting reforms already passed by Congress under the Biden-Harris administration. The questions will be whether stakeholders retain a voice and due process to enhance the quality and finality of federal actions, discouraging frivolous litigation, and whether the approval process will be made more efficient, coordinated, and transparent without watering down important environmental safeguards.

Energy markets are regulated markets, so the rules made by state regulators, independent regional grid operators, and the Federal Energy Regulatory Commission shape the market. To the extent that the new administration, despite the prospect of permitting reform, creates uncertainty about the objectivity, competence or transparency of executive agencies and federal rulemaking, investors will be wary.

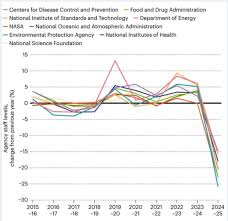

Agencies need institutional memory and rely on a specialized, expert workforce. Agencies that are understaffed or have unqualified political appointees will be unable to process approvals and permits quickly and properly, which they must do to advance development and reduce permit litigation risk. Agencies may be slow to issue guidance, for instance guidance on federal tax credits, or to promulgate new regulations contemplated or required by statute.

The new Trump administration may drag in approving new offshore wind projects or onshore wind or solar projects on federal land. Attrition among federal workers and attacks on civil service protections may create staffing shortages at the EPA, BLM, BOEM or other federal agencies. A lack of expertise or capacity at federal agencies or excess political influence over discretionary matters could significantly delay regulatory approvals, modify evaluation criteria, cloud the granting and clearance process for federal leases or rights of way, diminish the role of science in regulatory actions, or threaten the ability to defend already-permitted projects if they are legally challenged on environmental or other grounds.

Projects that are already permitted should be safe. The July 1, 2024 U.S. Supreme Court decision in Corner Post, Inc. v. Board of Governors of the Federal Reserve System, however, extended the deadline for challenging agency actions under the Administrative Procedure Act. The Court held that the statute of limitations period does not begin to run “until the plaintiff is injured by final agency action.” That case may create new regulatory uncertainty or opportunities for litigation to challenge approvals even for projects that are already in place. It is not certain how the Department of Justice under the next Trump administration would defend such challenges. The new Congress may address this ruling as part of a permitting reform package in 2025.

Ironically, sudden substantive changes in administrative policy – such as slashing emissions rules mandated by the Clean Air Act or other environmental regulations – by a new Trump administration could run counter to the narrow latitude given to federal agencies by the U.S. Supreme Court, including justices Trump appointed during his first term. The Court’s conservative majority repealed the Chevron deference doctrine in Loper Bright Enterprises v. Raimondo on June 28, 2024 and narrowed regulators’ authority by introducing the “major questions” doctrine in its 2022 decision in West Virginia v. EPA. These rulings make it harder for the administration to change course radically or arbitrarily in interpreting or enforcing (or failing to enforce) existing statutes absent clear instruction from Congress.

U.S. Supreme Court justices and lower court judges appointed by Trump during his second term may cast further doubt on federal regulatory actions and the predictability of federal law enforcement, clouding the validity of permits and causing confusion about compliance requirements for energy companies and other businesses, large and small. Judicial decisions upending established administrative law precedents and traditional regulatory frameworks also contribute to regulatory uncertainty.

Risk as it relates to investment decisions is a matter of perception, and that perception for investors must be evaluated on a relative basis across global markets. One advantage of the U.S. market compared to other countries is low political risk, at least historically and compared to other advanced markets. Permitting processes (though often slow, to allow for thorough review and public input) are usually open and objective. The risks of asset expropriation or project cancellation are low. Contracts are respected and enforced. Courts fairly adjudicate disputes. Corruption exists but is usually rooted out. In short, the rule of law gives investors confidence.

After Trump’s November 2024 electoral victory, political risk in the United States just increased significantly in the eyes of foreign investors – the sponsors, constructors, infrastructure funds and banks that are traditionally key providers of capital for U.S. power and infrastructure projects. Even U.S. investors may find that political risk in the United States has increased, at least to the extent that there is now a risk of greater regulatory tension, political conflict, and jurisdictional battles between federal and state governments in the populous “blue” states.

In the 1990s, many energy companies from the United States, Canada, Japan, and Europe rushed to invest in emerging markets in part for higher real returns and in part because of perceptions that those other countries (many with entrenched, undemocratic governments) had fast growth trajectories with low (or low enough) political risk. When political risk increased, as in parts of Latin America or South Asia, foreign investors either fled or charged a costly risk premium for invested capital. When investors fear (rightly or wrongly) that a national government is unpredictable, biased, chaotic, or corrupt, perceived political risk chills investment.

Fiscal And Monetary Policy

Akin to political risk, dramatic changes in federal fiscal or monetary policy could hurt investments in U.S. energy and infrastructure projects and companies. The federal debt ceiling is suspended only through January 1, 2025. A new federal tax bill is expected to be debated in 2025, when many of the tax changes enacted in 2017 expire. If federal tax revenues are reduced or the 2017 tax cuts extended without a corresponding reduction in federal spending, then there could be strong political pressure to curtail or end the tax credits that currently benefit energy investments. Given the magnitude of the federal deficit, closing the gap without raising significant revenue would necessitate large cuts in defense spending and in popular entitlement programs like Social Security and Medicare, which may be politically untenable.

Changes in federal income tax rates affect the efficacy of the tax credits that are used to stimulate investment. Reducing corporate tax rates would indirectly but significantly hurt investments that depend on tax credits for profitability. Lower corporate income tax rates (like recessions) mean less demand for tax shields and less value from tax credits. When a project sponsor receives less value from tax credits or, due to reduced demand for credits, pays more to monetize them, the company has a gap in its capital stack. Filling that gap requires additional debt or equity capital due to the inability to fully utilize the expected benefit from the tax credits. As such, the sponsor faces a higher cost of capital, less effective leverage, and a lower return on equity.

Shifting the income-tax based federal tax system to reliance on tariffs at scale, as proposed by President-elect Trump during the campaign, would be inflationary, reducing economic output while cutting tax receipts and increasing federal debt as a share of GDP. In that situation, the U.S. Treasury would have to increase the volume and pace of debt issuance, and bond markets would face downward pressure on bond prices. The Federal Reserve would likely have to increase short-term interest rates to combat renewed inflation. Taken together, these steps could increase long-term interest rates, which determine the cost of debt capital for energy investors. That combination of rising prices and rising rates would increase the cost of long-term, capital-intensive energy and infrastructure projects while reducing equity returns and valuations. A vicious cycle emerges. Project costs rise, equity returns fall, demand slows, credit spreads or risk premiums widen, and the dollar strengthens, further chilling new investment.

Federal Reserve Chair Jerome Powell’s term ends in May 2026. Central bank independence is a lynchpin of effective monetary policy and key to the dollar’s status as a reserve currency, which keeps the cost of government borrowing down. If the Federal Reserve is politicized and no longer seen as independent by financial markets or by other central banks, the ability of the U.S. government to finance expansion of the federal debt and to address business cycles, manage inflation, and maintain full employment would be jeopardized.

Market Impact

High tariffs, fiscal deficits, resulting inflation and interest rate pressures, under-resourced agencies, and uncertain tax, labor, and environmental policies, among other new challenges, could make development and investment in U.S. projects more expensive, riskier, and harder to finance. If so, energy investments will suffer.

The impacts of these changes would not be immediate. They would be measured in years not months. Near term, expect financial markets to react with their customary optimism about the prospect of looser regulation over the next four years. Expect investors relying on tax credits or federal regulatory approvals in the medium-term to become more cautious, given uncertainty over what comes next. Energy investments are capital-intensive and have long lead times. Valuations and returns depend on discounted cash flows forecasted ten to thirty years into the future. Long-term planning requires confidence in economic and regulatory stability.

It remains to be seen whether the next Trump administration will in fact constitute an inflection point in energy markets and policy or, like his first term, have a less lasting impact.

About Guest

Legal Planet welcomes contributions from policy partners and professors from other environmental law programs.…

READ more

Reader Comments