Who Should Own Our Electric Utilities?

Voters in Maine rejected a ballot initiative to buy out private utilities, but the campaign reflects a growing interest in public power.

This week voters in Maine rejected a ballot measure to implement a public takeover of the state’s two investor-owned utilities. The measure proposed acquiring the two investor-owned utilities that distribute 97% of Maine’s electricity and operating them as a new publicly-owned utility called Pine Tree Power, that would be governed by an elected board. 70% of Mainers voted to reject the measure and 30% supported it (as of this posting).

Electric Utility Models

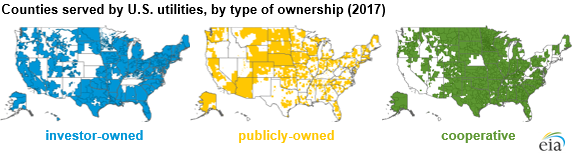

Electric utilities deliver electricity to customers. Utilities usually own and maintain the lines through which electricity travels. Rather than have many overlapping sets of lines from competing electricity companies running though the same neighborhoods, states grant monopolies to utilities to operate in particular areas. There are three main utility models in the United States: investor-owned utilities (IOUs), publicly-owned utilities, and member-owned or cooperative utilities. IOUs serve 72% of utility customers nationally, but there are many more publicly-owned utilities and coops than IOUs.

Investor-owned utilities are regulated to prevent them from taking advantage of their monopoly to gouge ratepayers. Publicly owned-utilities, on the other hand, have their rates set by the publicly-accountable officials (either elected or appointed) that run the utility. Here in Los Angeles, for example, one of the largest publicly-owned utilities in the country, the Los Angeles Department of Water & Power, is governed by five commissioners appointed by the mayor and confirmed by the city council. The adjacent investor-owned utility, Southern California Edison, has its rates regulated by the California Public Utility Commission.

Publicly-owned utilities have generally outperformed IOUs on rates and reliability. An evaluation of rates between publicly versus privately-owned utilities in Florida found that publicly-owned utilities provided lower rates for residential and small commercial customers, while privately-owned utilities provided lower rates for industrial and large commercial customers. These conclusions were affirmed nationally by a Public Power Association report that analyzed Energy Information Administration data. Here in California, IOUs have also been found to impose higher rates than municipally-owned utilities. In terms of reliability, a 2018 Energy Information Administration analysis found that municipally-owned utilities had fewer outages and outages for shorter durations than IOUs or cooperatives.

Tough Transitions

This week’s Maine ballot initiative was fueled by the fact that its two major investor-owned utilities are particularly unpopular, but this kind of campaign is not unprecedented. Although most of the country’s approximately 2,000 publicly-owned utilities were formed in the early 20th century, 50 new public power utilities have been formed in the past 30 years. These transitions have usually occurred at the municipal or county scale, rather than statewide like in the Maine proposal.

So how does a public takeover of an IOU actually work? Uncertainty and concern about the process is one reason some Maine voters rejected the proposal. Municipalization can take a few different paths. Some states require referendums prior to acquisition. Cities have acquired IOUs through purchase at a negotiated price, like in Jefferson County, Washington. More often though, the existing IOU inflates its price to make this impossible and localities have acquired them through condemnation proceedings, as in Hermiston, Oregon.

Many more cities have considered or unsuccessfully attempted municipalization in recent years. In 2019, city officials in San Jose and San Francisco, explored a public takeover of PG&E, another particularly unpopular IOU, but did not pursue it. In 2020, Chicago conducted a municipalization feasibility study that determined municipalization would not be financially feasible due primarily to the cost of severing the IOU’s infrastructure in Chicago with the rest of its infrastructure. In Michigan, Ann Arbor recently conducted a study to explore a transition from its existing IOU to a newly formed municipally-owned utility. Back in 2002, the California City of Corona attempted (unsuccessfully) to acquire the local infrastructure and operation of Southern California Edison through eminent domain. Even some of the unsuccessful or incomplete attempts, however, resulted in concessions for ratepayers by the IOUs. A feasibility study in Wichita, Kansas, for example, provided leverage that generated $28 million in rate relief.

Persistent Interest in Public Power

Multiple factors have elevated public power campaigns in recent years. First, a critique that the incentive structure for investor-owned utilities is misaligned with decarbonization goals has been gaining steam. In response, some advocacy has focused on rewriting the laws that regulate IOUs to change these incentive structures, but transitioning private companies to public ownership can accomplish this as well. The publicly-owned utility model also provides a (potentially complimentary) counterpoint to the distributed system of individual private ownership that a growing contingent of the rooftop solar industry is advocating. Incentives aside, consumers in some parts of the country have stronger preferences about the composition of their generation sources than in the past in light of climate change. In the Maine campaign, as in other recent municipalization processes, bringing more renewable generation online more quickly was a key concern.

Second, customers are increasingly unhappy with their utilities. One customer satisfaction survey cites rising bills as the recent driver of dissatisfaction in Maine and across the country. Stagnant wages and increased awareness about income inequality may exacerbate frustrations about high rates imposed by for-profit monopolies. At the same time, the combination of an aging grid and more frequent climate-related weather events have increased outages across the country in recent decades.

In addition to saving ratepayers money and reducing power outages, the Pine Tree Power campaign in Maine focused on bringing the power system under local control. Both of Maine’s investor-owned utilities are owned by foreign companies—Central Maine Power by Avangrid, a subsidiary of the Spanish company Iberdrola, and Versant by Canadian ENMAX. The desire to have more control and accountability over a range of decisions beyond just rates parallels increasing interest in energy democracy.

Despite the Pine Tree Power proposal’s failure and the concerns about the long and challenging acquisition process, the campaign was taken seriously by the IOUs, which pumped millions into advertising. Needless to say, they far outspent the grassroots campaign (by almost 40 to 1). The Pine Tree Power campaign instead featured yard signs and a song and music video by a Maine singer-songwriter with lyrics like, “Got a freezer full of venison / sump pump runs all night / I worry some wind blowing through the wires / puts out the light.”

The Maine ballot initiative was a clear loss for public power. But the loss is unlikely to put to rest the underlying tensions driving ratepayers around the country to wonder about the potential of publicly-owned utilities. The need to decarbonize the grid will only become more important and climate change is likely to put increasing strain on resilience and rates. The Maine campaign has elevated the issue of public power and may catalyze more action in the many jurisdictions where ratepayers are fed up with their IOUs.

Reader Comments

2 Replies to “Who Should Own Our Electric Utilities?”

Comments are closed.

About Ruthie

Ruthie Lazenby (she/her) is the Shapiro Fellow in Environmental Law and Policy at UCLA School of Law for 2023-2025, where her work will focus on energy law and regulation…

READ more

The author’s assertion that “publicly-owned utilities have generally outperformed IOUs on rates” relies on simple rate comparisons in the linked sources that fail to recognize that IOUs pay income and property taxes that must be passed on in rates while POUs are tax-exempt and also benefit from tax-exempt financing. Determining the more publicly beneficial form of ownership is a more complicated proposition than the author acknowledges, which may have been a factor in Maine voters’ rejection of the Pine Tree Power initiative.

Equating the metrics of existing consumer-owned utilities with the takeover of an entire utility (or, as was the case in Maine, 2 utilities) makes a false equivalence. Existing utilities did not inherit aging infrastructure built by someone else (in the case of Maine, spread out over three service territories,one of which not connected to the other two or the NEngland grid), did not need to recover a huge buyout cost, or pay an O&M provider. Such a takeover with similar ingredients has only happened once, forming the Long Island Power Authority. Maine, like LIPA, would have endured years of uncertainty until the buyout price was determined and the deal closed, followed by rates burdened with the added costs noted earlier. After 24 years of operation, LIPA has the highest rates in the region, and its customer satisfaction is as bad as Maine’s utilities. Proponents in Maine based their claims of reduced costs entirely on unsupported assertions that cheaper non-profit financing would make up for added costs.

It’s a disservice to Maine voters and their judgment to dismiss the results as due to the huge amounts spent in opposition. This was a voting population already deeply dissatisfied with their incumbent utility and angry at being bombarded with ads every hour of the day. Yet they did understand the risk and uncertainty with the referendum and voted “no” more than 2 to 1.